Last Updated on April 19, 2026 by Ecologica Life

Imagine you are the finance minister of a country already struggling under a heavy external debt burden. Economic shocks, rising global interest rates, or even natural disasters have pushed your finances to the limit. Every year, a large share of national income flows abroad simply to keep up with repayments.

Then an unexpected proposal appears. A creditor offers to reduce part of that debt, but with one unusual condition: the savings must be invested in protecting the country’s forests, oceans, or wildlife.

At first, the offer sounds almost too good to be true. Why would lenders forgive debt in exchange for environmental commitments? And what exactly do they expect in return?

This is the idea behind debt-for-nature swaps—financial agreements that convert sovereign debt into funding for conservation. Over the past few decades, countries from Bolivia to Seychelles and Ecuador have experimented with these deals, raising an important question: are they a genuine tool for protecting ecosystems, or simply another way to restructure debt under a greener label?

Table of Contents

A Planet in Crisis, Countries in Debt

Many countries that host the world’s most valuable ecosystems face a difficult reality. Rainforests, coral reefs and biodiversity hotspots are often located in developing economies that are also carrying heavy debt burdens.1

As climate change accelerates and environmental pressures increase, governments are forced to make difficult choices about how to allocate limited resources. Protecting forests, oceans and wildlife is expensive. At the same time, debt repayments to international creditors can consume a large share of national budgets.2

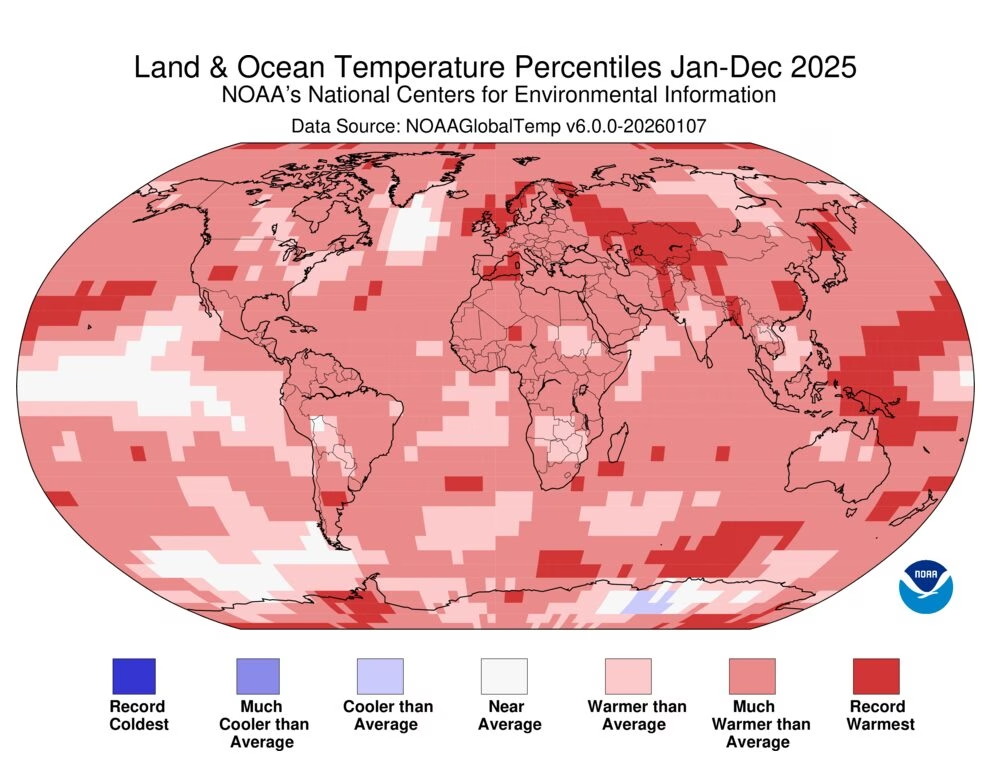

The timing could hardly be worse. Global temperatures continue to rise, with recent years among the warmest ever recorded. Scientists warn that the window to limit global warming to 1.5°C above pre-industrial levels is narrowing rapidly.3 Climate and environmental risks are now consistently ranked among the most serious global threats in the coming decade.

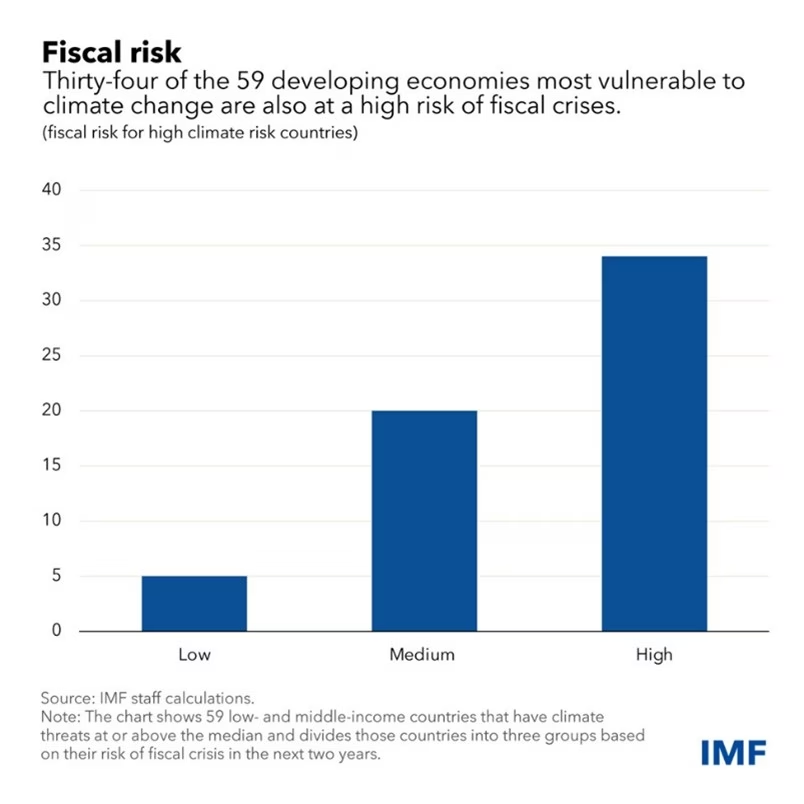

Yet many countries most exposed to climate change have the least financial capacity to respond. 4Higher global interest rates and tighter lending conditions have made borrowing more expensive, while existing debts have become harder to manage.5 In this environment, environmental programmes are often one of the first areas to face cuts.

This raises an important question: is it possible to reduce debt while protecting nature at the same time?

One solution that has gained renewed attention is the debt-for-nature swap.

What are Debt-for-Nature Swaps?

Debt-for-nature swaps are financial agreements that allow countries to reduce part of their external debt in exchange for committing funds to environmental protection.6

The idea first emerged during the debt crises of the 1980s. Many developing countries had borrowed heavily during the 1970s, but rising interest rates and falling commodity prices made repayment difficult.7 Governments under financial pressure often turned to resource extraction such as logging, mining or fishing to generate revenue. Environmental scientist Dr Thomas Lovejoy observed that debt pressure was indirectly driving environmental destruction.8 If countries were forced to exploit natural resources to service debt, then addressing the debt problem might also help protect ecosystems. This observation led to the creation of addressing a specific debt system: Debt-for-nature swaps.9

How the Mechanism Works

Debt-for-nature swaps generally fall into two categories depending on who holds the debt: private lenders or other governments.10

Private Debt Swaps

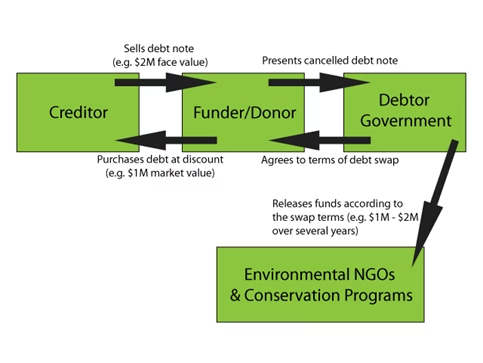

In a private swap, a country owes money to commercial banks or investors. An environmental organisation or financial intermediary then purchases part of that debt on the secondary market often at a discount.11 The private version can be understood by imagining a library fine that has grown so large the borrower cannot realistically pay it back. Instead of the library demanding full repayment, a third party steps in to buy the fine at a reduced price. The borrower then agrees to repay a smaller amount, but the money goes toward supporting the library rather than settling the original fine.

This approach was common in earlier debt-for-nature swaps, especially during past debt crises, and is often called a three-party arrangement because it involves the original lender, the country and the environmental organisation.12 In some cases, the library may even hand over the fine for free, knowing it will be put to good use.

In financial terms, the country agrees to redirect funds that would have gone to creditors into conservation projects at home. Because the debt was purchased at a discount, the same amount of money is set aside specifically for environmental programmes while reducing the country’s financial burden.13

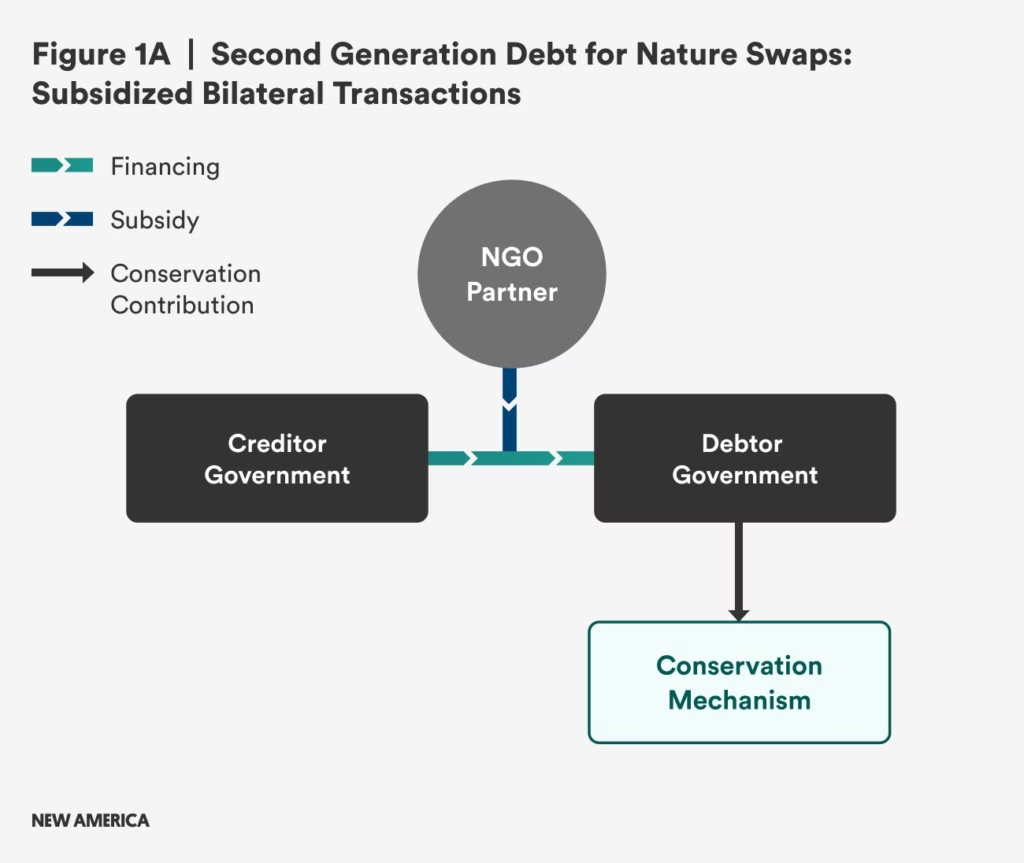

Public (Government-to-Government) Swaps

Public debt-for-nature swaps follow a simpler version of the same idea. In this case, a creditor country agrees to cancel or restructure part of another country’s debt on the condition that the savings are invested in environmental protection.14

Using the library fine analogy, this is the moment when the library itself decides to step in and change the rules. Instead of a third party buying the fine, the library agrees directly with the borrower to reduce or cancel part of it.

Because the agreement is negotiated directly, there is no intermediary buying the debt. However, the outcome is the same. A portion of the country’s financial obligations is transformed into funding for conservation.15

Why the Idea is Returning

Debt-for-nature swaps received relatively little attention during the early 2000s. At the time, large international debt relief initiatives reduced financial pressure on many developing countries, while global interest rates remained relatively low.16

In recent years, however, the situation has changed. The economic impact of the COVID-19 pandemic, rising borrowing costs and geopolitical uncertainty have placed new pressure on many emerging economies.17 At the same time, the urgency of climate and biodiversity protection has become more widely recognised.18

In this context, debt-for-nature swaps are being reconsidered as a way to link financial restructuring with environmental investment.19

Case Studies

Bolivia: Pioneering Debt-for-Nature

The first debt-for-nature swap took place in 1987 in Bolivia. Environmental organisation Conservation International purchased $650,000 of Bolivian debt on the secondary market for around $100,000.20

In return, Bolivia committed to protecting approximately 3.7 million acres of rainforest by establishing new conservation areas.21 This early experiment showed that even modest financial interventions could translate into tangible conservation outcomes.

Although the financial value of the deal was relatively small, it demonstrated that restructuring debt could be linked directly to environmental outcomes. The agreement also helped establish a model that would later be used in other countries.22

Some critics argued that the swap provided limited relief for Bolivia’s overall debt burden and raised questions about the influence of foreign organisations in national conservation decisions.23 Supporters, however, note that the government maintained control over land management while securing protection for large areas of rainforest that might otherwise have faced exploitation.24 Even if the financial relief was modest, the swap proved that debt-for-nature arrangements can deliver meaningful, lasting environmental benefits while balancing international support with national sovereignty.

Seychelles: Turning Ocean Debt into Conservation

A more recent example comes from Seychelles, a small island nation in the Indian Ocean that relies heavily on tourism and fisheries.25

Following a debt crisis in 2008, Seychelles worked with The Nature Conservancy to restructure part of its external debt. In 2016, around $21.6 million owed to members of the Paris Club of creditor nations was converted into a conservation agreement.26

Under the deal, Seychelles committed to protecting large areas of its marine territory and to investing in sustainable ocean management. A new institution, the Seychelles Conservation and Climate Adaptation Trust, was created to manage conservation funding.27

By 2020 the country had expanded protected marine areas to more than 30% of its waters, demonstrating how debt restructuring could support long-term environmental goals.28

The Galapagos Bond: The World’s Largest Private Swap

One of the largest debt-for-nature transactions to date occurred in 2023 in Ecuador. The deal focused on protecting the unique ecosystems of the Galapagos Islands, one of the world’s most famous biodiversity hotspots.29

Through a complex financial arrangement often referred to as the “Galapagos Bond,” Ecuador repurchased around $1.6 billion of its existing debt at a significant discount. The transaction generated approximately $656 million in new financing and will provide at least $12 million annually for conservation activities.30 The agreement supports the protection of a large marine reserve and a migratory corridor used by sharks, whales, sea turtles and other marine species.

The bond is supported by an $85 million credit guarantee from the Inter-American Development Bank and $656 million of political risk insurance from the U.S. International Development Finance Corporation to mitigate part of the credit risk. Financial guarantees from international development institutions helped reduce risk for investors and made the transaction possible.31

As with earlier swaps, some observers questioned whether such deals prioritise investor security or create long-term financial obligations. By relying on international banks and guarantees, critics argue that Ecuador structured the deal to make investors feel safe, rather than pushing for deeper debt relief.32 But these criticisms overlook what the Galapagos bond actually achieved.

Environmental commitments under the Galapagos Bond were embedded in legally binding frameworks with dedicated oversight mechanisms, making it more difficult for future administrations to quietly abandon conservation goals.33 The transaction allowed the country to buy back debt at a steep discount while securing dedicated, long-term funding for ocean protection that would not have existed otherwise. At the time, Foreign Minister Gustavo Manrique Miranda described biodiversity as a new form of “currency,” highlighting the country’s innovative approach to linking conservation and finance.34

Lessons from Bolivia, Seychelles, and the Galapagos

From the first Bolivian forests to the world’s largest private swap in Ecuador, debt-for-nature deals demonstrate a simple but powerful idea: debt doesn’t have to drain resources, it can be leveraged to save the planet.

Taken together, these examples illustrate how financial mechanisms can support environmental goals. Debt-for-nature swaps transform existing obligations into investments in conservation, allowing governments to redirect resources toward protecting ecosystems.35

They are not a universal solution. The scale of global environmental challenges far exceeds what swaps alone can address, and each deal requires careful negotiation to ensure transparency, national sovereignty and community involvement.36

However, they do demonstrate an important principle: financial systems do not have to operate separately from environmental protection. Under the right conditions, they can reinforce it.

Food for Thought: Saving the Planet or Selling it Off?

Debt-for-nature swaps inevitably raise difficult questions. Some critics worry that such agreements could allow wealthier nations or financial institutions to exert influence over how natural resources are managed.37 Others argue that they address the symptoms of global debt rather than the underlying causes.38

These concerns deserve serious consideration. Environmental protection must ultimately be guided by local priorities and long-term economic stability.39

At the same time, the alternative is often a continuation of the status quo: countries under financial pressure relying on resource extraction to meet debt obligations.40 From Bolivia’s pioneering forests to Seychelles’ coral reefs and Ecuador’s Galapagos waters, these deals turn debt into a lifeline for ecosystems that might otherwise be lost.

Debt-for-nature swaps are not a silver bullet. But they represent an innovative attempt to rethink how finance interacts with the natural world.

When the choice is between ecosystems collapsing under debt or finance being used to protect them for the long term, the answer should not be a controversial one.

This is not about selling nature off, it’s about finally pricing its survival into the system. When designed carefully, debt-for-nature swaps show that debt can be a positive tool for both the planet and its people — and that’s where our focus should be.

- World Bank (2023) International Debt Report 2023. Washington, DC: World Bank. ↩︎

- Ibid, 1. ↩︎

- Intergovernmental Panel on Climate Change (2023) AR6 Synthesis Report: Climate Change 2023. Geneva: IPCC. ↩︎

- United Nations Development Programme (2022) Debt-for-nature swaps and sustainable development. New York: UNDP. ↩︎

- International Monetary Fund (2023) Global Financial Stability Report. Washington, DC: IMF. ↩︎

- WWF (1987) Debt-for-Nature Swaps: A Conservation Tool for Developing Countries. Washington, DC: World Wildlife Fund. ↩︎

- World Bank (1989) World Debt Tables: External Debt of Developing Countries. Washington, DC: World Bank. ↩︎

- Thomas Lovejoy (1989) Aid debtor nations’ ecology. Science, 243(4890), pp. 291–292. ↩︎

- IUCN (1988) Debt-for-Nature Swaps: A Guide for Conservation Action. Gland: International Union for Conservation of Nature. ↩︎

- Ibid, 1. ↩︎

- IMF (2022) Debt-for-Climate Swaps: Analysis, Design, and Implementation. IMF Working Paper No. 2022/162. Washington, DC: International Monetary Fund. ↩︎

- OECD (2023) Financing Climate and Nature: Debt Conversion and Innovative Instruments. Paris: OECD Publishing. ↩︎

- Debt Justice (2025) Debt-for-nature swaps reduce debt seven times less than debt restructurings. ↩︎

- Blended Finance Taskforce (2023) Debt Swaps for Climate and Nature: Scaling Up Impact. London: Systemiq. ↩︎

- Nature Conservancy (2022) Debt Conversion for Conservation: How Debt Swaps Work in Practice. ↩︎

- UN DESA (2020) World Economic Situation and Prospects. New York: United Nations Department of Economic and Social Affairs. ↩︎

- IMF (2024) Global Debt Monitor: Rising Risks in Emerging Markets. Washington, DC: International Monetary Fund. ↩︎

- IPCC (2023) AR6 Synthesis Report: Climate Change 2023. Geneva: Intergovernmental Panel on Climate Change. ↩︎

- World Resources Institute (2023) Debt Swaps for Climate and Nature: Scaling Up Finance for Biodiversity. Washington, DC: WRI. ↩︎

- Conservation International (2022) Debt-for-Nature Swaps: History and Impact. Washington, DC: Conservation International. ↩︎

- UNEP (2022) State of Finance for Nature. Nairobi: United Nations Environment Programme. ↩︎

- OECD (2023) Financing Climate and Nature: Debt Conversion and Innovative Instruments. Paris: OECD Publishing. ↩︎

- Debt Justice (2025) Debt-for-nature swaps and their effectiveness in debt reduction. ↩︎

- World Economic Forum (2024) Debt-for-nature swaps and sovereign climate finance mechanisms. ↩︎

- Climate Policy Initiative (2023) Global Landscape of Climate Finance 2023. ↩︎

- The Nature Conservancy (2021) Seychelles Debt Conversion Project: Ocean Conservation Outcomes. ↩︎

- World Economic Forum (2024) Blue finance and debt-for-nature swaps: scaling ocean conservation finance. ↩︎

- High Ambition Coalition for Nature and People (2022) Marine Protection and Debt Conversion Case Studies. ↩︎

- IUCN (2023) Protected Area Financing and Debt-for-Nature Innovations. Gland: International Union for Conservation of Nature. ↩︎

- Inter-American Development Bank (2023) Galapagos Marine Conservation and Debt Conversion Initiative. Washington, DC: IDB. ↩︎

- Ibid, 30. ↩︎

- Debt Justice (2025) Debt-for-nature swaps: risks, benefits and limitations. ↩︎

- Nature Conservancy (2023) Ecuador Galapagos Debt Conversion: Financing Ocean Protection. ↩︎

- Reuters (2023) Ecuador says biodiversity is “currency” in landmark debt swap. ↩︎

- Columbia Center on Sustainable Investment (2024) Debt Conversion and Sustainable Development Finance. New York: Columbia University. ↩︎

- UNCTAD (2024) Debt Sustainability and Climate Finance in Emerging Markets. Geneva: United Nations Conference on Trade and Development. ↩︎

- Shandra, J.M., Shandra, C.L. and London, B. (2023) Environmental Governance and Global Inequality. New York: Routledge. ↩︎

- Eurodad (2024) Debt Swaps and Climate Finance: A Critical Assessment. Brussels: European Network on Debt and Development. ↩︎

- African Development Bank (2024) Debt and Climate Vulnerability in Africa: Policy Pathways. Abidjan: AfDB. ↩︎

- International Institute for Environment and Development (IIED) (2024) Nature Finance and Sovereignty: Governance Risks in Debt-for-Nature Swaps. London: IIED. ↩︎